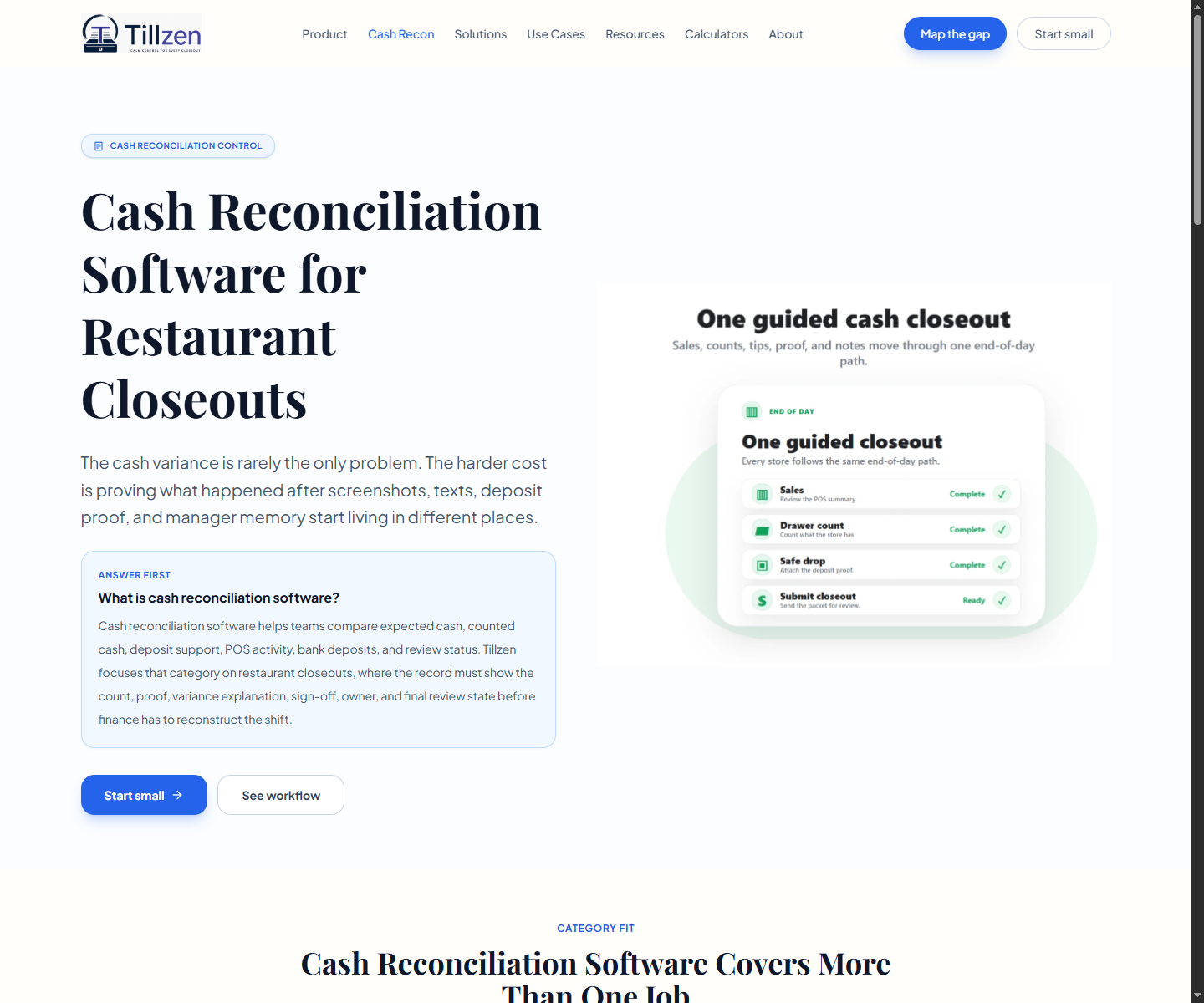

How does accounting Should Not Have to Rebuild the Day work?

A daily sales report can look complete and still leave accounting with work that should have been preserved at close.

The POS total is there. The bank deposit is somewhere else. The void reason lives in a manager note. The shortage explanation was sent by text. The bookkeeper can still reconcile the account, but the daily record did not make the review easy.

This guide is for that handoff. It defines the record a restaurant should keep before the accounting team has to clean up the month.

- Accounting review gets easier when the daily source record is stronger.

- The issue is not reconciliation. It is the quality of the record behind it.

- The goal is a record that survives the handoff from store to books.

How does the Missing Layer Between POS and the Books work?

Most restaurant accounting resources explain reconciliation, chart-of-account cleanup, software connections, or month-end processes. Those are useful, but they often start after the daily evidence has already drifted.

The missing layer is the accountant-ready record. It shows the day in a way that a bookkeeper, controller, or advisor can review without asking the store to recreate what happened.

That makes the resource useful for accounting firms because it gives clients a concrete upstream standard, not a vague instruction to send cleaner information.

This fills the accounting-resource gap between daily sales reports and the downstream reconciliation work that depends on them.

What Belongs in the Daily Sales Record?

The record should preserve the facts accounting needs to understand the day. It should not be a folder of disconnected screenshots. It should tie the operating record to the financial review path.

A complete record gives the reviewer enough details to decide whether the day is clean, explainable, open, or blocked.

- POS close summary for the store, date, shift and drawer or cash source.

- Expected cash, counted cash, deposit amount, card batch details and cash difference.

- Deposit proof or proof status for each cash deposit you review.

- Void, comp, refund, payout, discount and adjustment details where relevant.

- Manager sign-off, accounting reviewer, owner, current state and final resolution.

Why Reconciliation Still Breaks With Good Software?

Accounting software can organize the books. POS exports can move totals. Bank feeds can show deposits. None of those explain why a shortage happened, why a deposit proof is missing, or who owns an open issue.

That is why the daily record matters. It keeps the operating explanation beside the accounting input while the manager can still remember the shift.

- A bank match can confirm an amount without explaining the store details.

- A POS total can show activity without proving the deposit record is complete.

- A journal entry can clean the books without teaching the store what failed.

- An easy-to-check record lets accounting and operations work from the same facts.

How do teams separate normal Differences From Review Problems?

Restaurants have timing differences. Cash deposits may land later. Card batches may settle in a different way. Tips, refunds, delivery channels and paid-outs can create normal accounting work. The record should separate normal timing from weak records.

That separation is important because the accounting team should not have to treat every mismatch like a mystery. Some items need a normal reconciliation note. Others need manager follow-up, proof repair, or ownership.

- Timing difference: expected and explainable from the record.

- Proof problem: deposit support is missing, delayed, unclear, or disputed.

- Cash Difference problem: counted cash differs and the reason is weak or absent.

- Ownership problem: the record shows an issue but no one owns the next step.

How does client Intake Questions for Accounting Firms work?

Before an advisor recommends cleanup work, they can ask for a few daily records. The goal is to inspect the source record, not to judge the whole accounting function from one month-end report.

Good intake questions make the conversation more productive because they show the client where the missing details starts.

- Can you show a daily sales record for one ordinary day and one issue day?

- Can the record show deposit proof without searching email or messages?

- Can it explain voids, comps, refunds, discounts, paid-outs and cash difference?

- Can accounting see who signed, who reviewed and what remains open?

- Can final resolution be found next month without asking the manager again?

How to Use the Record Before Month End?

The record should be reviewed while the day is still close enough to explain. A lightweight daily or weekly review catches missing proof, vague notes and open owners before they become month-end cleanup.

The review does not need to create a long meeting. It needs to mark the record clean, partial, open, or blocked and route the next action.

- Clean: accounting can review from the record.

- Partial: one field exists but needs clarification.

- Open: an issue has a named owner and due date.

- Blocked: proof, explanation, owner, or final state is missing.

How does a Practical Standard for Restaurant Teams work?

Restaurant teams do not need to become accountants to improve the handoff. They need a daily record that keeps accounting inputs and operating details together. That is a manager behavior problem, a record-design problem and a review-path problem at the same time.

When the record improves, accounting can spend less time chasing facts and more time reviewing the work that belongs to accounting.

- Managers preserve the record while the shift is fresh.

- Bookkeepers receive a cleaner source record.

- Controllers can see open issues before they become recurring cleanup.

- Owners can compare stores by record quality, not by dollar cash difference.

What should I read next about the Accounting Handoff?

Use this record as the source-record standard. Pair it with narrower Tillzen resources when the issue is proof, cash difference investigation, or broader closeout control.

- Read /resources/restaurant-accounting-closeout-control-guide for advisory framing.

- Read /resources/deposit-proof-and-sign-off-workflow for proof-state review.

- Read /resources/restaurant-cash-variance-investigation-guide for over-short triage.

- Read the cash reconciliation software page when the daily sales packet needs counts, deposit proof, cash-gap notes and review owners in one record.

- Read /resources/restaurant-closeout-reviewability-standard-white-paper for the neutral record standard.

What does the Same Deposit, Two Different Records look like?

Two stores can both deposit 2,100.00 and create very different accounting outcomes. Store A attaches the deposit proof, shows expected and counted cash, explains a small overage and names the reviewer. Store B shows the same deposit amount but leaves the receipt in a camera roll and explains the difference later by text.

The bank may match both deposits. Accounting may reconcile both days. But Store A gave the team an easy-to-check source record, while Store B created a reconstruction task.

That distinction is the point of the record. The accounting outcome is not whether the books can be reconciled. It is whether the store record made reconciliation cleaner and coaching easier.

- Same deposit amount, different record quality.

- A matched bank deposit does not show the source record was complete.

- Accounting should be able to see proof and explanation in one record.

- The stronger record creates a better coaching signal for operations.

How does adjustment Details Accounting Should See work?

Adjustments are where daily sales records often become fragile. A void, comp, refund, delivery correction, cash paid-out, manual tip change, or discount may be legitimate, but the later reviewer needs to know why it happened and who approved it.

The daily record should not bury those events in a POS report with no explanation. It should preserve the adjustment type, amount, reason, approver and review follow-up. If the answer belongs with payroll, HR, legal, or tax review, the record should route it instead of pretending the issue is closed.

This helps accounting firms because it gives clients a practical way to distinguish bookkeeping questions from store-process questions.

- Record the adjustment type and amount.

- Write a manager reason that another person can understand.

- Preserve who approved the adjustment and who reviewed it later.

- Route sensitive or open questions to the right owner before closeout is marked final.

How does weekly Review Without Creating a New Bureaucracy work?

A useful weekly review should be small. Pull records with missing proof, repeated cash difference, unclear adjustments, open owners, or late final states. Review those records first instead of rereading every clean day.

The purpose is to spot repeat patterns. One missing receipt may be a store habit. Repeated vague cash difference notes may be a training issue. Open owner fields across several stores may mean the review path is not clear.

The accounting team can use the review to improve the input standard without taking over store operations.

- Review issue records before clean records.

- Group issues by proof, cash difference, adjustment, owner and final state.

- Decide whether the first repair is training, record design, routing, or timing.

- Measure whether fewer records need off-system follow-up after the repair.

What the Record Does Not Claim?

The record does not replace accounting judgment, tax review, payroll review, legal review, bank reconciliation, or POS controls. It does not claim every shortage is preventable or every missing receipt is suspicious.

Its job is narrower and more useful: preserve the daily facts so the right reviewer can work from the same record. That boundary is important for accountants because it keeps the resource practical, credible and safe to send to clients.

The cleanest promise is simple. Better records give accounting cleaner inputs and give restaurant teams clearer coaching signals.

- No legal, tax, payroll, or fraud-detection guarantees.

- No claim that accounting software or POS systems are replaced.

- No invented ROI number or universal savings claim.

- The standard is useful without booking a sales call first.

Reference sources

Which public sources support this guide?

These public references support the recordkeeping, cash-control and tip-record context used across Tillzen resources. Tillzen does not give legal advice.

How do you turn the record into a rollout decision?

Map the current record, pick the first stores and measure whether review gets cleaner before rollout expands.

The work is real: 18 quick-service stores, 1,400+ hours given back annually, $1M+ in tip dollars reviewed annually, 18,000+ store closes annually and 3+ years supporting them.

- quick-service stores

- 18

- hours given back annually

- 1,400+

- tip dollars reviewed annually

- $1M+

- store closes annually

- 18,000+

- years supporting them

- 3+