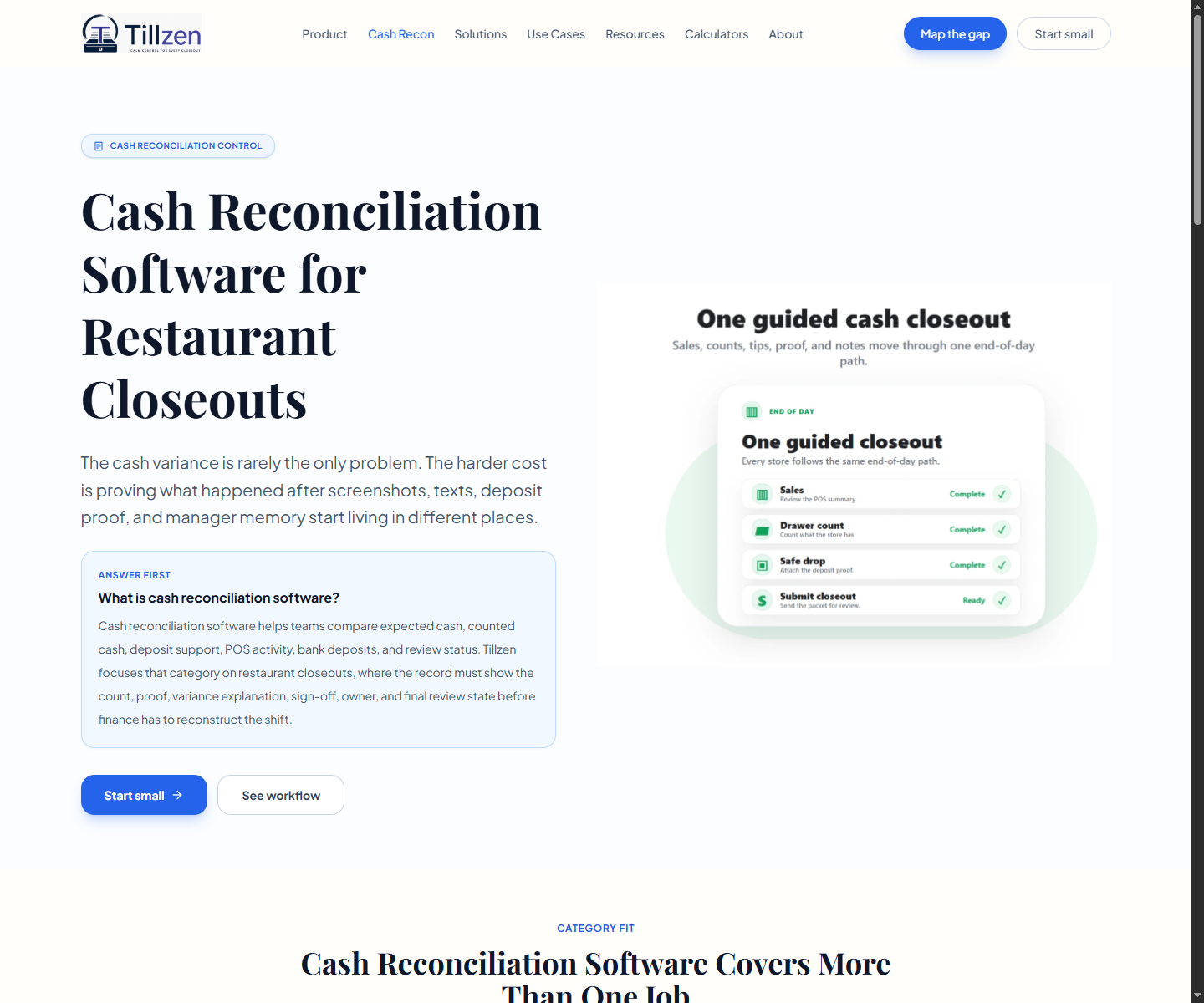

How does the Shortage Is Not the First Problem work?

A cash difference has a way of making everyone tense. The number is small enough to feel annoying and large enough to demand an answer. So the conversation often jumps straight to blame.

That jump is the mistake. A cash difference is not one problem. It can be missing proof, bank timing, a drawer count issue, a tip adjustment, a process miss, or a repeat pattern finally becoming visible. Treating all of those as the same thing makes review louder and less useful.

This guide slows the moment down. First classify the cash difference. Then decide who owns it. Then preserve the answer where the next reviewer can find it.

- Missing proof is different from missing cash.

- Timing is different from theft.

- A repeat pattern is different from a one-off closeout mistake.

How do teams make the Record Do the Awkward Work?

The cleanest cash difference process is not the one with the harshest follow-up. It is the one where the record carries enough details that the reviewer does not have to interrogate the store.

If the record shows the drawer, expected amount, counted amount, proof status, reason, owner and final resolution, the conversation changes. It becomes specific. It becomes calmer. It becomes about the next action instead of someone's memory from last night.

That is why this guide works for finance and advisory review. It gives teams a practical triage path without pretending every over-short issue has the same cause.

Use this when finance review needs a concrete issue-review path instead of another broad cleanup discussion.

Why Cash Difference Review Starts Too Late?

Cash difference review gets expensive when it starts after shift details are gone. The visible shortage or overage may be small, but the missing explanation, proof and owner create the cleanup work.

The investigation starts with record quality, not blame.

The strongest review path starts from the original closeout record. Finance should see the expected cash, counted cash, proof status, manager note, sign-off and current review follow-up before deciding how serious the cash difference is.

- The expected cash number is separated from proof.

- The first manager explanation is vague or missing.

- Finance and operations start from different records.

- The same issue repeats without a visible owner.

How do teams separate evidence Gaps From Cash Gaps?

Not every cash difference is a true cash problem. Some cases are evidence problems. A missing receipt, unclear deposit image, blank note, or unsigned closeout can make a record impossible to trust even when the drawer may be correct.

That distinction changes the route. Evidence gaps go back to the store or district owner. True cash gaps may need manager review, cashier review, deposit review, or escalation under the team's policy.

- Evidence gap: the record cannot support the submitted closeout.

- Cash gap: counted cash and expected cash do not match.

- Timing gap: the money belongs to another shift, day, or deposit event.

- Process gap: the pattern repeats by store, drawer, or manager.

How does classify Cash Difference Before Routing Review work?

Classification keeps the work proportional. A small overage with clear proof may need logging. A shortage above threshold with no explanation needs a different path. A repeated pattern needs review even when each case is small.

The classification should remain visible in the record so operations and finance understand why the issue moved to a specific owner.

- Inside threshold and documented: log and monitor.

- Missing proof: route to the proof owner.

- Unexplained shortage or overage: assign district review.

- Repeated pattern: escalate according to written policy.

- Resolved case: preserve the explanation and close review.

How do teams build the Escalation Queue by Cause?

The escalation queue should not be a single list of problems. A cash shortage, missing proof, unclear timing, repeated store pattern and vague manager note do not need the same owner.

Classifying the cause keeps the route proportionate. It also gives finance and operations one shared reason for why a case was logged, routed, watched, or escalated.

- Evidence cases route to the proof owner.

- Cash gaps route by threshold and policy.

- Timing gaps route to the person who can match the event.

- Repeat patterns route to district or ownership review.

What Advisors Can Take From This Guide?

Finance and advisory conversations often speak to controls at a high level. This guide gives teams a concrete cash difference triage path when restaurant clients need cleaner daily inputs before accounting review.

The reader value is a practical issue path, not a broad finance claim.

The page is strongest when linked from content about outsourced accounting, restaurant finance operations, over-short review, or month-end cleanup. It turns the topic into a daily record problem.

- Review angle: separate evidence gaps from cash gaps.

- Buyer angle: controller, bookkeeper, fractional CFO, or finance advisor.

- Store angle: reduce the morning cash difference chase.

- Pilot angle: measure routed cases across two to five stores.

What should I read next about cash Difference Review?

Use this guide after the daily closeout record is defined and deposit proof status is visible. The cash difference review is as strong as the record it starts from.

- Read /resources/restaurant-daily-closeout-checklist to define packet completeness.

- Read /resources/deposit-proof-and-sign-off-workflow to reduce proof cases.

- Read /resources/restaurant-accounting-closeout-control-guide for advisory handoffs.

- Use /run-pilot to test cash-gap routing in a 14-day pilot.

How do teams build a Cash Difference Triage Table Before Investigation?

Cash Difference investigation works best when the first step is classification, not accusation. A reviewer should know whether the case is a cash shortage, cash overage, delayed proof issue, timing mismatch, drawer-transfer issue, refund or void details gap, or repeat process pattern before anyone starts assigning blame.

A triage table makes the first review faster because it separates the questions that require finance from the questions that require store details. It also helps district leaders coach from patterns instead of individual surprises. If three stores have the same proof pattern, that is a process problem. If one drawer has repeated unexplained shortages, that is a different escalation path.

This is the kind of store detail that finance advisory sites seldom include. They often describe cash difference as an accounting symptom. This resource gives them a practical way to route the symptom while the store memory is still fresh.

- Classify the case before asking for more details.

- Use separate states for cash error, proof error, timing error and explanation error.

- Track repeat patterns by store, manager, drawer and daypart.

- Send open or high-confidence issues to the next reviewer.

How does evidence Questions for Every Over-Short Case work?

A cash difference note is useful when it helps the next reviewer understand what changed and what remains unknown. A note that says drawer short is not enough. The reviewer needs the count, expected amount, proof status, manager explanation, transaction clue and owner for the next action.

The best investigation format is short but structured. It asks what was counted, where the difference appeared, whether deposit proof supports the count, whether the manager observed a specific event and whether this case resembles a prior pattern. That structure protects managers too, because the review becomes evidence-led instead of personality-led.

For readers, this section gives outsourced accounting and finance teams a client-safe checklist. It does not promise that every cash difference can be solved. It shows how to preserve enough details for a fair review.

- What amount was expected and what amount was counted?

- Is deposit proof attached, missing, delayed, or unclear?

- Did the manager provide a specific event, transaction, or timing explanation?

- Has this pattern appeared for the same store, drawer, manager, or daypart before?

How to Separate Coaching Cases From Control Cases?

Not every cash difference should become a disciplinary conversation. Some cases show training needs, some show weak record design and some show a control issue that requires escalation. Mixing those paths creates noise and makes managers less likely to write useful notes the next time.

A coaching case often has a clear store explanation and no pattern of repeat issues. A control case often has missing evidence, vague notes, repeated open shortages, or conflicting proof. The reviewer should decide which lane the case belongs in before the follow-up starts.

That distinction matters for multi-unit restaurant teams because district managers have limited time. They need to know which cases deserve coaching, which deserve process repair and which deserve higher review. The record should make that decision easier.

- Coach when the explanation is specific and the record shows a fixable behavior.

- Repair process when proof or notes go missing across stores across stores.

- Escalate when the amount, pattern, or evidence gap exceeds the review threshold.

- Close when the final state and owner are preserved in the record.

How does twenty-One Day Cash Difference Review Starting Point work?

Before a pilot starts, capture a starting point that counts more than dollars. Track how many cash difference cases had clear proof, how many had specific notes, how many required off-system follow-up, how many were open after one business day and how many repeated at the same store.

After 14 days, compare the same measures. A useful pilot does not need to claim that cash difference disappeared. It needs to show whether fewer cases arrived without details and whether the ones that remained were easier to route. That is a stronger reader-value story because it is practical and believable.

For finance teams, the starting point turns cash difference investigation from a pile of issues into an operating report. It shows whether the review process is improving, even before the dollar trend is statistically meaningful.

- Measure cases the team can check on the first pass, not total cash difference dollars.

- Track missing proof and vague explanations as separate failure types.

- Compare open cases at day one, day seven and day 14.

- Use the result to decide whether to expand the control standard to more stores.

How does cash Difference Review Examples by Root Cause work?

A shortage with attached proof and a specific manager note should take a different path than a shortage with no proof and no explanation. The first case may need coaching or a quick transaction check. The second case needs evidence repair before anyone can make a fair judgment. The same dollar amount can create two very different stepss.

An overage can also be misleading. It may come from change-making error, a missed cash sale, a refund timing issue, or a deposit event that was recorded on the wrong day. If the reviewer treats every overage as good news, the process loses the chance to fix the underlying record problem.

Repeat patterns deserve their own lane. A single 12.00 shortage may be normal operating noise. A 12.00 shortage every Friday night at the same drawer is a control signal. The resource should teach reviewers to look for pattern, proof, owner and final state together.

- Shortage with proof: review the reason and decide whether coaching is enough.

- Shortage without proof: repair the proof status before closing the case.

- Overage with timing mismatch: match the event before assuming the store is clean.

- Repeat pattern: route to district review even when each single amount is small.

What Good Cash Difference Notes Sound Like?

A good cash difference note is factual, short and easy to check. It names the likely event, the evidence that supports it and the next action if the cause is not known. It avoids blame language and avoids generic phrases that cannot be checked.

For example, register two was short 18.00 after the 7 p.m. count is better than drawer off. It becomes stronger when the note adds that the manager found a voided cash ticket that may explain 15.00, attached the receipt and assigned the remaining 3.00 difference to review. The note does not need to solve everything. It needs to make the next review fair.

This type of guidance is worth citing because it gives finance and advisory audiences concrete language to use with clients. It helps them train better records without writing a restaurant-specific operating manual from scratch.

- Name the drawer, shift and amount.

- Name the likely cause when there is evidence.

- Attach the proof or mark the proof status.

- Assign the open amount instead of hiding it in a vague note.

How does escalation Thresholds Without Guesswork work?

Every restaurant leader needs thresholds, but the threshold should not be a dollar amount. A small amount with missing proof may deserve review. A larger amount with clear proof, specific explanation and fast owner assignment may be easier to close. The escalation model should combine amount, evidence quality, repeat pattern and open state.

A practical model can use three lanes. Monitor cases are low amount, complete proof and no repeat pattern. Review cases have missing proof, vague reason, or open owner. Escalate cases have higher amount, repeated pattern, conflicting evidence, or repeated missing details at the same store.

This prevents the team from ignoring small repeated problems and overreacting to one event with a clean explanation. It also gives finance and district leaders a shared decision rule.

- Monitor low-risk cases with complete records.

- Review cases with missing proof, vague notes, or open owners.

- Escalate repeated patterns or conflicting evidence.

- Use the lane to set response time and reviewer ownership.

Reference sources

Which public sources support this guide?

These public references support the recordkeeping, cash-control and tip-record context used across Tillzen resources. Tillzen does not give legal advice.

How do you turn the record into a rollout decision?

Map the current record, pick the first stores and measure whether review gets cleaner before rollout expands.

The work is real: 18 quick-service stores, 1,400+ hours given back annually, $1M+ in tip dollars reviewed annually, 18,000+ store closes annually and 3+ years supporting them.

- quick-service stores

- 18

- hours given back annually

- 1,400+

- tip dollars reviewed annually

- $1M+

- store closes annually

- 18,000+

- years supporting them

- 3+