How does month-End Cleanup Starts Earlier Than Month-End work?

The old accounting handoff waits too long to ask whether the daily record can explain itself.

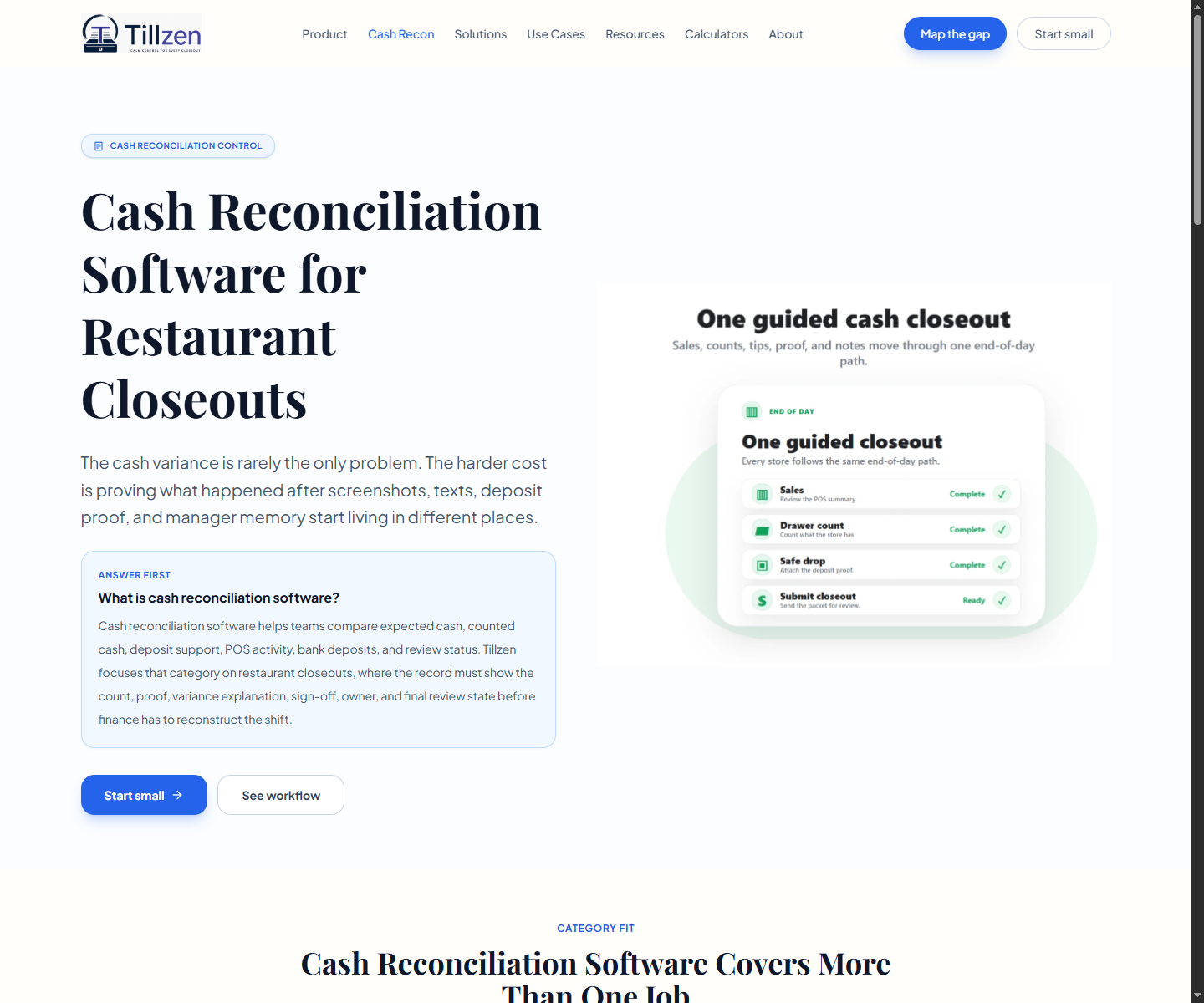

Accounting teams often meet the closeout problem after it has already hardened. The bank process is there. The POS report is there. The store summary is there. But the proof, cash difference explanation, manager sign-off and owner trail are scattered.

At that point accounting is not reviewing a clean source record. It is reconstructing one. That is slow for the advisor and frustrating for the restaurant leader because the missing details lived upstream all along.

This guide moves the conversation back to the daily record, where the cleanup problem often begins.

- The bookkeeper should not have to rebuild the shift.

- The controller should not have to chase proof after the record is stale.

- The store record should be easy to check before it reaches accounting.

How does give Advisors Something Useful to Send work?

An accounting firm does not need to sell Tillzen to make this resource useful. The stronger use is education. Send it when a restaurant client describes messy closeouts, missing receipts, vague cash difference notes, or too many month-end questions.

The guide gives the client a way to inspect the upstream record before the advisor recommends a cleanup project. That makes the relationship more productive because both sides can talk about the same daily evidence.

The result is a practical reference, not a product brochure.

This fills the advisory-content gap between month-end cleanup and the store-level records that create it.

Why Accounting Cleanup Starts Upstream?

Restaurant accounting cleanup often begins with a missing daily record. The books may be downstream, but the evidence lives upstream in store closeout behavior.

A closeout record makes the handoff easier by preserving proof, cash difference notes, sign-off and open ownership before the accounting team has to ask for it.

- Proof is attached before the record reaches accounting.

- Cash Difference notes are written while the details still holds.

- Managers know which issues remain open.

- Finance review starts from one record, not multiple message threads.

How does the Record Accounting Teams Need for Review work?

Accounting teams need cleaner inputs, not another place to chase the same unclear record. The closeout record should show enough details for review before accounting has to rebuild the shift.

That record gives advisors a practical way to discuss control without promising full transformation or replacing the team's existing POS and accounting stack.

- Expected and counted cash.

- Deposit proof and proof status.

- Cash Difference reason and review owner.

- Manager sign-off and timestamp.

- Final resolution state for easy to check review.

How Advisors Can Use This Guide With Clients?

Accounting partners can share it with clients without blaming the restaurant leader. It names the daily record gap and gives the advisor a reason to discuss control before month-end cleanup.

- Send it after a client mentions deposit or cash difference cleanup.

- Use it before proposing a process review.

- Anchor the next step on a 14-day pilot, not a broad migration.

- Keep claims tied to cleaner records and review ownership.

This is a stronger education asset than a generic software page for accounting partners.

How does set a Daily Input Standard for Month End work?

Month-end cleanup is often blamed on the end of the month, but the missing details starts in the daily close. Accounting teams need proof status, cash difference reason, signer, owner and resolution while the shift is still fresh.

This section gives accounting firms and advisory blogs a concrete client education angle: improve the daily record before asking accounting to rebuild it.

- Capture proof status before the deposit question ages.

- Require a usable cash difference reason at close.

- Name open owners before accounting review.

- Preserve final state for finance-ready reporting.

How does give Advisors a Client-Safe Framework work?

Advisors need resources they can send without turning the handoff into a broad software pitch. This guide frames the issue as closeout-control hygiene: a daily operating record that supports cleaner accounting inputs.

Elena's advisor framing stays finance-ready and easy to check without overclaiming.

That makes it practical for Restaurant365-style ecosystems, outsourced accounting teams and fractional CFOs working on restaurant store finance.

- Use it when clients chase deposit proof after the fact.

- Use it when cash difference explanations arrive through messages.

- Use it when restaurant teams need a small pilot instead of a migration.

- Use it before proposing a deeper process review.

What should I read next about accounting Partners?

Pair this guide with the cash difference investigation guide when the client has over-short issues. Use the deposit proof steps when the main issue is missing evidence.

- Read /resources/restaurant-cash-variance-investigation-guide for exception triage.

- Read /resources/deposit-proof-and-sign-off-workflow for evidence trails.

- Read /resources/cost-of-variance-2026-report for the business case.

- Read the cash reconciliation software page when the client needs counts, proof, cash-gap notes, owners and finance review in one closeout record.

- Map the current accounting handoff before scoping rollout.

Why Accounting Cleanup Should Move Upstream?

Accounting teams often receive the closeout record after the operating details has already gone cold. By then, a missing receipt, vague shortage note, or open deposit question becomes cleanup work instead of review work. The team can still reconcile the books, but the daily cause is harder to see.

The upstream fix is not to make accountants run store operations. It is to give stores a daily record standard that accounting can trust. The record should preserve the closeout identity, count, proof, cash difference reason, sign-off, owner and final state before the record reaches month-end work.

That makes the resource useful for advisory pages because it shows where the advisor can help the client improve inputs. It is not a generic accounting automation pitch. It is a practical explanation of how better daily records reduce downstream ambiguity.

- Move proof and issue details into the daily record.

- Keep manager sign-off separate from accounting review.

- Preserve open owners before month-end cleanup starts.

- Use daily record quality as an advisory diagnostic.

How does client Intake Questions for Advisors work?

Before recommending a tool or process change, an advisor can ask a few intake questions that reveal whether the issue starts upstream. Can the client show the closeout record for a specific store and date? Can they show proof status? Can they show who owned an open cash difference? Can they show final resolution without searching messages?

These questions keep the conversation grounded. A restaurant may say month-end is messy, but the cause may be daily closeout drift. Another client may have clean records but weak reporting. The advisor needs to know which problem they are solving.

For accountants and fractional CFOs, this section creates a direct client-use case. It gives them a repeatable intake checklist for restaurant clients.

- Ask for one recent clean closeout and one recent issue closeout.

- Check whether proof status is visible without a message search.

- Ask who owns open issues before accounting receives the file.

- Identify whether the client needs record control, reporting cleanup, or both.

How does month-End Problems That Start at Daily Close work?

Some month-end problems are daily closeout problems that accumulated without calling attention. Missing deposit proof, open over-short notes, unclear manager approvals and undocumented adjustments can all land on accounting after the store has moved on.

When that happens, accounting work becomes investigative. The team has to ask managers what happened, rebuild the proof status and decide whether the issue is cash, timing, or documentation. That is expensive because the details is late and scattered.

A closeout-control resource should help advisors explain this chain to clients. Better daily records do not replace accounting judgment. They give accounting better inputs so the judgment starts from a cleaner operating record.

- Missing proof becomes late reconciliation work.

- Vague cash difference notes become manager-interview work.

- Unclear sign-off becomes approval reconstruction.

- Unowned issues become delayed closeout cleanup.

How does advisor-Plain Pilot Report for Clients work?

An advisor-plain report should show whether the client improved the inputs that accounting receives. The report can include first-pass record completeness, proof volume, open issue ownership, follow-up messages and the number of records that reached accounting without enough details.

This keeps the pilot practical. The advisor does not need to claim that every closeout dollar changed. They need to show whether the daily operating record became easier to check, reconcile and explain.

That report can also become a client-retention asset. It shows the advisor is not cleaning up books after the fact. They are helping the restaurant build a cleaner operating record upstream.

- Starting Point and day-14 record quality by store.

- Missing proof and vague-note counts before and after.

- Open issues with named owners.

- Recommendation to expand, adjust, or pause based on input quality.

How does closeout Questions to Ask Before Month End work?

Before month end, accounting should not have to discover basic closeout gaps for the first time. The operating team should already know which stores are missing proof, which cash differences lack explanation, which sign-offs preserved open items and which issues still need an owner.

An advisor can help the client by turning those questions into a weekly review rhythm. The rhythm does not require the advisor to run daily operations. It makes the client surface incomplete records before they become accounting cleanup.

The strongest question is: can finance review this closeout without asking the store what happened? If the answer is no, the record still belongs in store repair before it becomes month-end noise.

- Which stores submitted incomplete records this week?

- Which proof cases are still open?

- Which cash difference notes are too vague to review?

- Which issues have no named owner before accounting close?

How Advisors Can Use the Guide With Clients?

An accounting firm can use this guide as a practical education asset for restaurant clients. The message is not that the firm sells software. The message is that cleaner daily records make the accounting relationship more productive for both sides.

In advisor conversations, the advisor can send the resource after a call where the client describes messy closeouts, missing receipts, or repeated month-end questions. The guide gives the client a concrete way to inspect the upstream record before the advisor proposes a cleanup project.

A deeper guide gives advisors enough substance to justify the link and enough practical structure to help a client self-diagnose.

- Use it after discovery calls with restaurant clients.

- Position it as an upstream-input checklist.

- Pair it with the deposit proof steps for evidence issues.

- Pair it with the cash difference guide for issue-heavy clients.

How does advisory Service Packaging for Closeout Control work?

An advisor can package closeout-control review as a small front-end engagement. The engagement does not have to be a large transformation project. It can be a record-quality assessment, a closeout record standard and a 14-day pilot report for two to five stores.

That packaging helps clients approve the work because the scope is specific. The advisor is not asking the restaurant to overhaul accounting. They are asking the restaurant to show whether daily closeout inputs can become cleaner before they reach accounting.

The package can also create a stronger advisory relationship. The firm moves from reactive cleanup to upstream control, while the client receives a practical operating artifact they can use with managers.

- Assessment: score current records and identify the weakest fields.

- Standard: define the minimum easy to check closeout record.

- Pilot: test the standard in a small store group.

- Report: recommend expand, adjust, extend, or stop.

Reference sources

Which public sources support this guide?

These public references support the recordkeeping, cash-control and tip-record context used across Tillzen resources. Tillzen does not give legal advice.

How do you turn the record into a rollout decision?

Map the current record, pick the first stores and measure whether review gets cleaner before rollout expands.

The work is real: 18 quick-service stores, 1,400+ hours given back annually, $1M+ in tip dollars reviewed annually, 18,000+ store closes annually and 3+ years supporting them.

- quick-service stores

- 18

- hours given back annually

- 1,400+

- tip dollars reviewed annually

- $1M+

- store closes annually

- 18,000+

- years supporting them

- 3+